BuddyBoss

20% off on annual plan

✅ Deal information :

✅ Deal information :

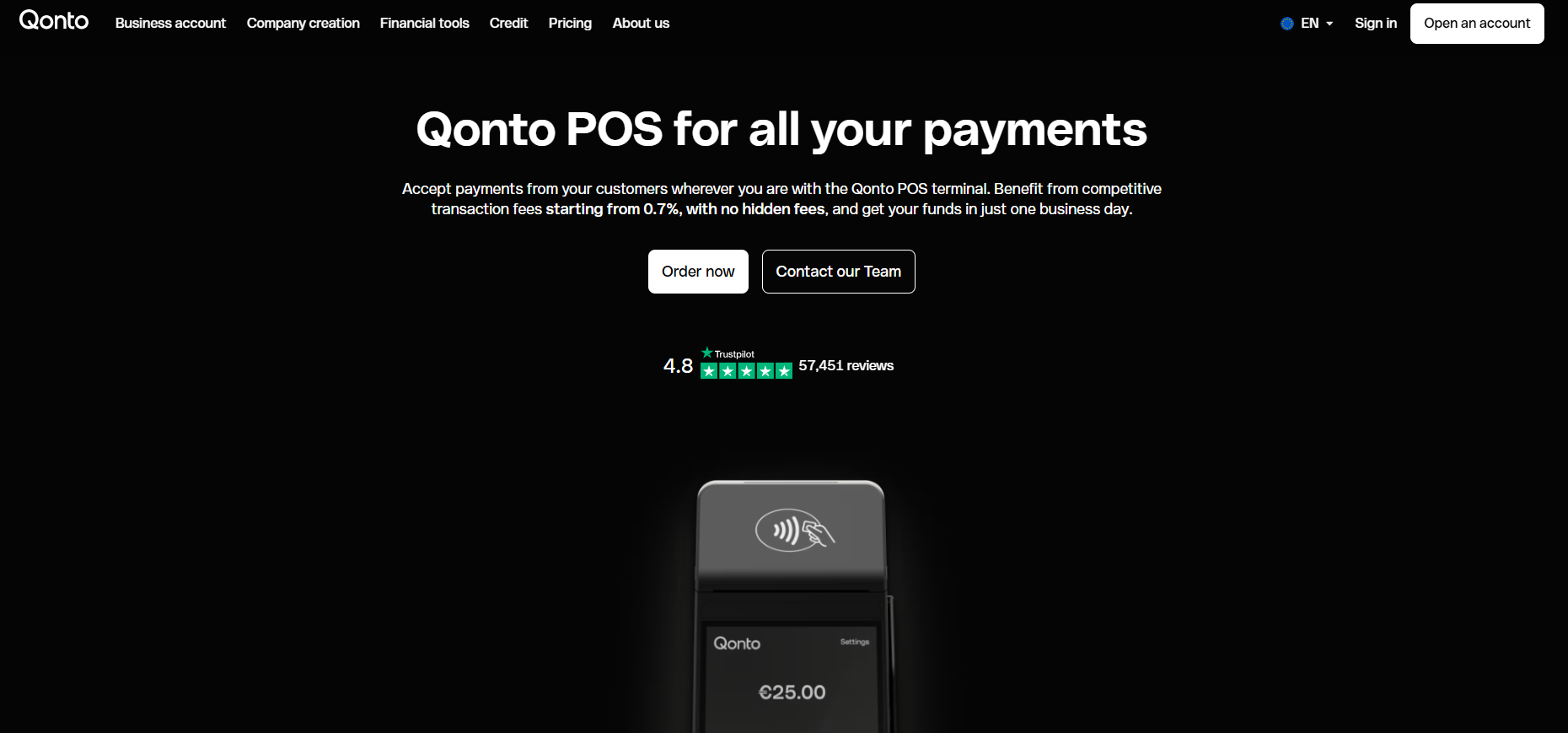

Qonto has expanded its business account with a payment collection solution designed for professionals who receive payments on the go. The Qonto payment terminal integrates natively with your bank account, which means that every transaction you receive appears in real time in your app—no need to juggle multiple tools. Funds are deposited into your main account as early as the next business day—a real advantage over traditional payment processors, which often have longer processing times.

In terms of fees, Qonto offers rates starting at 0.7% on payments made with European bank cards, whereas traditional providers typically charge 1.65% to 1.75% for this type of transaction. The terminal operates completely independently thanks to its built-in 3G, 4G, and Wi-Fi connectivity, without the need for a nearby smartphone, and it accepts both chip and contactless cards as well as mobile payments such as Apple Pay or Google Pay. This solution is particularly well-suited for entrepreneurs (tradespeople, ride-hailing drivers, service providers) rather than retail businesses requiring advanced point-of-sale software.

With Qonto, your card payments are directly integrated into your business account: no more juggling between a payment processor and your bank.

Choose from two terminals; there are no rental fees—you only pay for the device, plus a commission per transaction:

While you wait to receive your terminal (which comes pre-configured and ready to use), you can start accepting payments right away with Tap to Pay on iPhone and Android: your smartphone becomes a payment terminal.

Purchasing and Using the Qonto Payment Terminal: How Does It Work?

The Qonto mobile payment terminal, also known as a TPE, is a device that allows youto accept credit card payments from your customers, no matter where you are. It falls into the Smart POS category: it is standalone and operates without needing to be connected to a smartphone, unlike smaller mPOS-type readers.

The terminal connects to 3G, 4G, 5G, or Wi-Fi networks to transmit transactions; Bluetooth connectivity is not supported. It accepts payments via chip cards and contactless payments using NFC technology, as well as mobile wallets such as Apple Pay, Google Pay, and Samsung Pay. In short, it supports the payment methods your customers use every day.

One of the key features isnative integration with the Qonto business account. Every incoming payment is automatically synced to the app, complete with categorization and reconciliation, which eliminates the need for double entry and streamlines accounting tracking. You maintain a unified view of your incoming payments, expenses, and cash flow all in one place.

Payments are processed quickly: once a payment is received, it takes one business day for the funds to appear in your account, whereas some other solutions have longer processing times.

Qonto offers two models to suit your needs. The Pocket is compact, lightweight, and designed for professionals who travel frequently and want to accept payments anywhere. The Pro is more robust, features built-in receipt printing, and can handle a high volume of transactions, making it better suited for retail stores and restaurants. In both cases, the device comes preconfigured and is ready to use as soon as you turn it on.

While you wait for your terminal to arrive, you're not stuck: Tap to Pay technology on iPhone or Android turns your smartphone into a card reader, so you can start accepting payments right away.

In terms of security, the terminal complies with the PCI PTS v6 standard, one of the strictest in the industry. Any attempted intrusion locks the device, ensuring that the card reader and its software remain tamper-proof. Finally, orders are placed directly through the Qonto app, and customer support is available seven days a week via chat, email, or phone.

The pricing for the Qonto POS terminal is based on a simple model: a one-time purchase of the device, followed by a commission on each transaction, with no separate subscription fee for the terminal. Note that using the terminal requires an active Qonto business account, with subscriptions starting at €9 per month (excluding tax), which is therefore an additional cost.

Two terminals are available depending on your business needs: the Pocket, designed for mobility, and the Pro, which features receipt printing and is suited for higher transaction volumes. The table below summarizes the costs. The amounts shown are exclusive of tax.

| Service | Rates |

|---|---|

| TPE Pocket (one-time purchase) | 99 € (excluding tax) |

| TPE Pro (one-time purchase) | €199 (excluding tax) |

| European Credit Card Commission | starting at 0.7% per transaction |

| Subscription or Rental of the Device | No |

| Maintenance Fees and Minimum Billing Amount | No |

| Disbursement of Funds | Next business day (D+1) |

| Qonto Business Account | Required, starting at 9 € (excluding tax) per month |

1️⃣ If you are a freelancer or consultant:

Square offers a mobile card reader paired with an app—a lightweight solution that’s well-suited for one-time payments during appointments or on-site services. Shine integrates payment processing features into its business account, which is convenient when you want to use a single tool for both banking and payments. Stripe can also meet this need through payment links and mobile contactless payments—a flexible approach for those who primarily invoice for services and occasionally accept payments in person.

2️⃣ If you are a startup:

Stripe stands out for its comprehensive ecosystem, which integrates online payments, physical terminals, and recurring billing within a single infrastructure, featuring an API that’s popular with technical teams. Mollie focuses on simplicity and multi-method support to accept a wide range of payment methods internationally. Payplug covers both online sales and point-of-sale payments, a useful combination for a business that sells across multiple channels. These solutions are well-suited for a growing business that needs to streamline its payment flows.

3️⃣ If you are a small business or an SME:

Square offers a more comprehensive payment processing solution—ranging from mobile card readers to point-of-sale hardware—tailored for businesses that handle high transaction volumes and want structured sales management. Payplug is suitable for retailers with both brick-and-mortar and online stores, offering an omnichannel approach. Sellsy integrates invoicing, payment processing, and CRM into a single suite, which appeals to organizations that want to link customer relationship management with their financial operations. The choice will depend on your transaction volume and the level of integration you seek with your other tools.

Otherwise, these other software programs may also be a good alternative to Qonto - Payment Terminals.No resources currently available.